Vacancy pattern real estate opportunity types are defined as the distinct investment categories that emerge when specific vacancy behaviors, by property class and market condition, signal underpriced or distressed assets. The U.S. Census Bureau reported rental vacancy at 7.3% in Q1 2026, a figure that looks stable on the surface but masks sharply different dynamics across multifamily, industrial, office, and retail sectors. Investors who treat vacancy as a single metric miss the real signal. The pattern behind the number, how long a unit sits empty, why it went vacant, and what the local credit environment looks like, determines which opportunity type you are actually looking at. This article maps those patterns to specific investment strategies using 2026 data from CoStar, Apartments.com, and the U.S. Census Bureau.

1. Vacancy pattern real estate opportunity types by property class

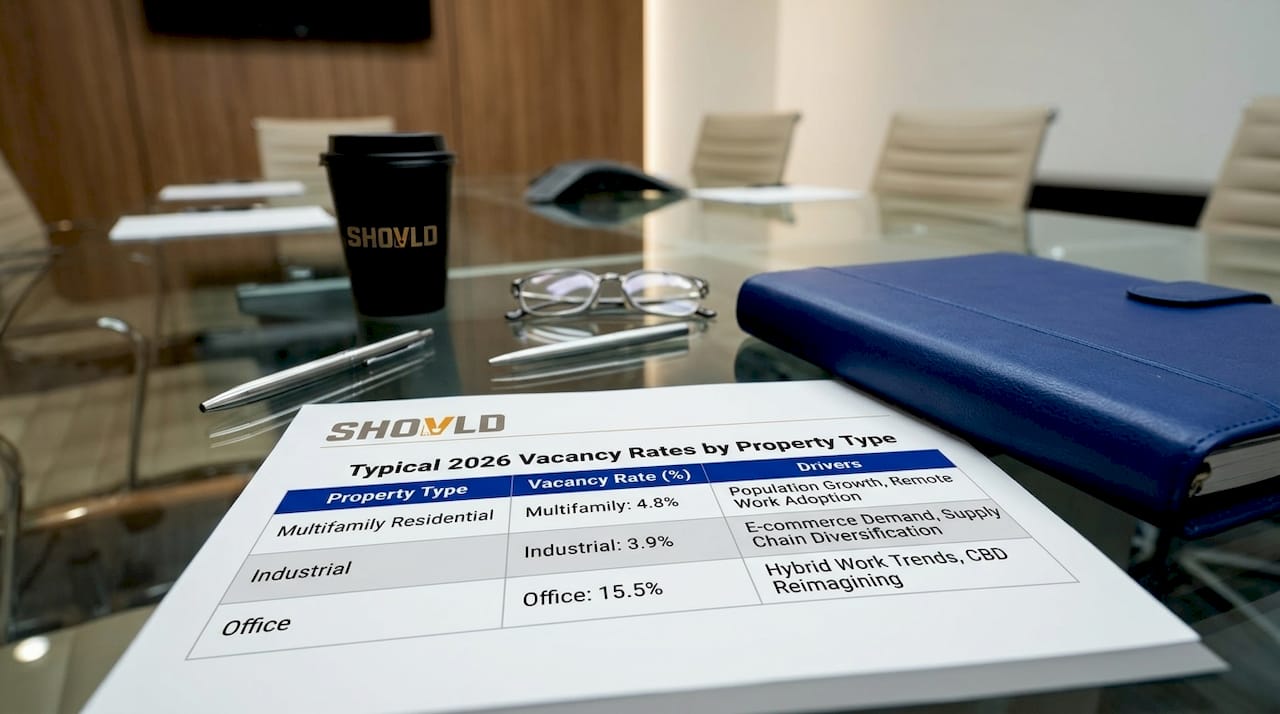

Different property types produce fundamentally different vacancy patterns, and each pattern points to a different class of investment opportunity. Understanding the baseline for each sector is the starting point for any serious real estate market analysis.

| Property Type | Typical 2026 Vacancy Rate | Primary Vacancy Driver |

|---|---|---|

| Multifamily residential | ~8.8% (late 2026) | Oversupply from construction pipeline |

| Industrial | ~7.8% (peak 2026) | Supply-driven, demand stabilizing |

| Retail | Varies widely by submarket | Tenant mix and e-commerce pressure |

| Office | Elevated in major metros | Remote work and lease expirations |

Multifamily is under the most acute pressure right now. Multifamily vacancy is projected to reach 8.8% nationally in late 2026 before easing in 2027, driven by a surge of new units delivered into markets that have not yet absorbed prior supply. That oversupply condition creates a specific opportunity type: lease-up plays where a motivated seller needs to exit before stabilization.

Industrial vacancy tells a different story. Industrial vacancy is forecasted to peak at 7.8% in 2026 with rent growth near 1.0%, then improving through 2027. This is a supply-driven peak, not a demand collapse, which means the opportunity type is a timed acquisition before the recovery cycle compresses cap rates again.

2. How vacancy loss differs from vacancy rate

Physical vacancy rate and vacancy loss are not the same number, and confusing them is one of the most common underwriting errors in distressed property analysis.

Physical vacancy rate measures the percentage of units or space that is unoccupied at a given moment. Vacancy loss is calculated as vacant space multiplied by the rent amount multiplied by the vacancy period, expressing the actual dollar income lost rather than just the percentage of empty units. A 10% vacancy rate on a 100-unit apartment building sounds manageable. If those units sit empty for six months at $2,000 per month each, the vacancy loss is $1.2 million. That is the number that matters for underwriting.

Economic vacancy goes further still. Economic vacancy includes bad debt, concessions, and non-revenue units that reduce effective gross income beyond what physical vacancy captures. A property showing 94% physical occupancy can still carry 15% economic vacancy when you factor in free-rent concessions and delinquent tenants. This gap between headline occupancy and actual income is where forced sales originate.

Pro Tip: When evaluating a distressed acquisition, always build a vacancy loss model that separates physical vacancy, concession costs, and bad debt into three distinct line items. Sellers almost never present economic vacancy in their offering memorandums.

Vacancy downtime also varies significantly by property type due to leasing frictions and tenant improvement costs. An industrial building can sit vacant for 12 to 18 months while a tenant negotiates a build-out. A multifamily unit typically re-leases in 30 to 60 days. That difference in downtime directly changes the vacancy loss calculation and the risk profile of the acquisition.

3. Opportunity types that emerge from distressed vacancy patterns

Specific vacancy patterns generate specific investment opportunity types. Mapping the pattern to the opportunity is the core skill in distressed property analysis.

-

Forced sale opportunities. Rising vacancy linked to credit and refinancing stress increases foreclosure and forced sale risk. When a property's vacancy loss exceeds its debt service coverage, the owner faces a liquidity crisis. These assets surface as off-market sales, note purchases, or REO acquisitions at significant discounts.

-

Value-add renovation targets. Properties with elevated vacancy caused by deferred maintenance or functional obsolescence, not market softness, represent value-add plays. The vacancy pattern here shows high turnover and short tenancies rather than long-term empty units. Renovation restores competitiveness and compresses vacancy back to market levels.

-

Lease-up and repositioning plays. Newly constructed or recently converted properties with high vacancy but strong submarket fundamentals are lease-up opportunities. The vacancy is temporary and structural, not distress-driven. The investor's return comes from the spread between the acquisition price at high vacancy and the stabilized value once the property reaches market occupancy.

-

Long-term hold stabilizations. Some vacancy patterns signal a property that is simply mismanaged rather than fundamentally impaired. Below-market rents, poor marketing, and weak property management create artificial vacancy. These assets stabilize quickly under competent ownership and are best held for cash flow rather than flipped.

"Headline occupancy metrics can mask underlying risks. Credit stress requires underwriting with vacancy buffers and realistic unpaid-rent allowances." — Investing Plus analysis on credit stress and real estate

Underwriting errors that ignore financing terms and vacancy timing can convert manageable occupancy problems into liquidity crises. This is the mechanism behind most forced sales in distressed property segments, and it is the signal that experienced investors learn to read before the market does.

4. Geographic and market segmentation effects on vacancy patterns

Vacancy rates and the opportunity types they generate are not uniform across U.S. markets. Location and local policy create material differences in both the pattern and the play.

Sun Belt multifamily markets, including Atlanta, Austin, and Phoenix, absorbed the largest share of new construction in 2024 and 2025. U.S. rents have fallen for 33 consecutive months as excess multifamily inventory continues to pressure vacancy rates and rents. That sustained rent decline in oversupplied Sun Belt submarkets creates forced sale conditions for developers who underwrote 2021 rent growth assumptions.

Urban coastal markets face a different dynamic. Office vacancy in cities like San Francisco and Chicago remains structurally elevated due to remote work adoption and lease expirations. The opportunity type here is adaptive reuse conversion, not traditional office investment. Investors who understand construction project timing relative to vacancy cycles can position for conversion plays before the crowd identifies them.

| Market Type | Dominant Vacancy Pattern | Primary Opportunity Type |

|---|---|---|

| Sun Belt multifamily | Oversupply-driven high vacancy | Forced sale acquisitions |

| Urban office | Structural long-term vacancy | Adaptive reuse conversion |

| Industrial suburban | Cyclical supply peak | Timed acquisition pre-recovery |

| Suburban residential | Policy-influenced vacancy | Value-add or hold |

Vacancy taxes in West Coast cities reduce speculation but do not fully eliminate vacant units because of conversion costs and rent levels. This means policy-driven vacancy pressure creates motivated sellers in specific submarkets, particularly in Seattle and Portland, where the tax burden adds to carrying costs without guaranteeing a viable exit.

Pro Tip: Before targeting a submarket, check whether a vacancy tax or rent control ordinance is in effect. Both policies change the seller's motivation and the buyer's exit strategy in ways that standard cap rate analysis will not capture.

5. Tools and strategies for vacancy pattern analysis

Effective property investment strategies built on vacancy patterns require more than pulling a vacancy rate from a data terminal. The analytical framework matters as much as the data source.

-

Vacancy loss modeling. Vacancy loss modeling extends the vacancy rate by incorporating downtime and rent replacement assumptions to better reflect income impact. Build a model that runs three scenarios: base case at market vacancy, stress case at 15% above market, and recovery case at stabilization. The spread between stress and recovery defines your return corridor.

-

Signal intelligence platforms. Shovld tracks permits, code violations, HOA pressure, distressed-property indicators, and municipal records across multiple U.S. markets. The platform scores opportunities before they surface in traditional listing channels, which is the timing advantage that separates early movers from the crowd. Investors using Shovld's signal intelligence can identify vacancy-driven distress signals weeks or months before a property hits the market.

-

Loan term and maturity analysis. Properties with loans maturing in 2025 or 2026 that were originated at low interest rates face refinancing stress when vacancy is elevated. Pulling loan maturity data from public records and cross-referencing it with vacancy trends identifies the forced sale pipeline before it becomes visible.

-

Rent replacement assumptions. Never underwrite a distressed acquisition using the seller's in-place rents. Build your own rent replacement schedule based on current market comps, concession levels, and time-to-lease by unit type. This is where most buyers leave money on the table or, worse, overpay.

-

Due diligence on economic vacancy. Request trailing 12-month rent rolls, not just current occupancy. Look for concession patterns, delinquency trends, and non-revenue units. These data points reveal whether the vacancy pattern is improving or deteriorating, which determines whether you are buying at the bottom or catching a falling asset.

Key takeaways

Vacancy patterns are the most reliable early indicator of forced sales, value-add targets, and lease-up opportunities across every major property class in 2026.

| Point | Details |

|---|---|

| Vacancy loss vs. vacancy rate | Always model dollar vacancy loss, not just the percentage rate, to capture true income impact. |

| Property type drives pattern | Multifamily oversupply and industrial supply peaks create different opportunity types requiring distinct strategies. |

| Geographic segmentation matters | Sun Belt forced sales, urban adaptive reuse, and policy-driven West Coast vacancies each demand a tailored approach. |

| Economic vacancy reveals real risk | Bad debt, concessions, and non-revenue units can push economic vacancy well above physical vacancy. |

| Signal timing is the edge | Identifying vacancy-driven distress before it reaches the market is the primary competitive advantage in 2026. |

Why most investors read vacancy patterns too late

I have spent years watching investors pull the same CoStar report everyone else pulls and wonder why they are always competing on price. The problem is not the data. It is the timing and the depth of interpretation.

The investors who consistently find the best distressed opportunities are not smarter. They are earlier. They are reading vacancy loss trends at the property level, not the market level, and they are cross-referencing those trends with loan maturity schedules and code violation histories. That combination tells you which owner is six months from a forced decision before the owner knows it themselves.

The 2026 multifamily data is a perfect example. Everyone sees the 8.8% national vacancy headline. The investors who act on it profitably are the ones who have already mapped which specific properties in which specific submarkets are carrying economic vacancy above 20% with a loan maturing in Q3. That is not a market call. That is a property-level signal, and it requires a different analytical toolkit than what most investors are using.

The other mistake I see constantly is treating vacancy rate as static. Vacancy patterns move. A property trending from 5% to 12% vacancy over 18 months tells a completely different story than one that has held at 12% for three years. The direction and velocity of the pattern matter as much as the current number.

— Avi

See vacancy-driven opportunities before the market does

Shovld is built for investors and analysts who want to act before the market reacts. The platform aggregates permits, code violations, distressed-property indicators, and municipal records across U.S. markets, then scores each signal so you can prioritize the opportunities most likely to convert.

For vacancy pattern analysis specifically, Shovld surfaces properties showing deferred maintenance signals, HOA pressure, and permit activity that correlates with owner distress, often weeks before a listing or a foreclosure notice appears. If you are serious about building a distressed property pipeline that does not depend on what everyone else is already looking at, Shovld gives you the early visibility that changes how you source deals. Explore the platform and see which signals are active in your target markets today.

FAQ

What is a vacancy pattern in real estate?

A vacancy pattern is the observable trend in how long, how often, and why a property or property class experiences unoccupied space over time. Investors use these patterns to classify opportunity types ranging from forced sales to value-add acquisitions.

How does vacancy loss differ from vacancy rate?

Vacancy rate measures the percentage of empty units at a point in time, while vacancy loss calculates the actual dollar income lost by multiplying vacant space by rent and vacancy duration. Economic vacancy adds concessions and bad debt on top of physical vacancy.

What vacancy rate should concern a real estate investor?

Any vacancy rate trending upward over 12 to 18 months warrants deeper analysis, particularly when combined with rent concessions or loan maturity pressure. The specific threshold varies by property type, with multifamily stress becoming visible above 10% in most markets.

Which property types have the highest vacancy risk in 2026?

Multifamily carries the highest near-term risk, with national vacancy projected at 8.8% in late 2026 due to oversupply. Industrial vacancy is also peaking at approximately 7.8% but is expected to recover through 2027 as supply normalizes.

How can investors identify forced sales from vacancy patterns?

Cross-reference elevated vacancy trends with loan maturity schedules and code violation records. Properties with rising economic vacancy and near-term debt maturities are the most likely candidates for forced sales, often before any public listing or foreclosure filing appears.

Recommended

- The Construction Industry Has a Timing Problem: Why Contractors Enter Too Late and Miss 80% of Opportunities | Shovld Blog

- The South Florida HOA Crisis: How Property Owners Are Drowning in Repairs While Contractors Miss Opportunities | Shovld Blog

- Angi and Thumbtack Aren't Dead — But a New Model Is Taking Over Construction Lead Sourcing | Shovld Blog

- Shovld Blog | Construction Signal Intelligence & Market Insights